In the first article we started off by having a look at the big picture. In last week’s article we drilled further down into the details of iron ore. This week’s article will be on the seaborne coal trade. In subsequent reports we will drill further down into the other commodity groups of grains, minor bulks and bauxite before we finish off with a look at the supply side.

The coal share in total dry bulk trade measured by volume was 27%* in 2019 and was as such the second largest commodity group (see left graph below). The demand for vessels cannot simply be derived from volume – we need to take distance and trade inefficiencies into account as well – as time spent on the total transport work is what ultimately impacts the aggregated demand for vessels. If we measure the coal share in total dry bulk trade by using the Dwt x Duration metric (more details here), we end up with coal having a 23% market share in dry bulk vessel demand in 2019 (see middle graph below). In the first nine months of 2020 the market share of coal has decreased to 21%.

If we break it down by segment, we see that 46% of all seaborne coal volumes are carried on Panamaxes (see right graph below), with the Cape segment in second place at 28% and Supras in third place at 20%. If we pivot and instead look at the market share of coal in each vessel segment, we see that while 28% of all seaborne coal is carried on Capesize vessels, only 21% of Capesize demand is derived from carrying coal. So, given this slightly asymmetrical relationship you could argue that the coal trade is more dependent on the Capesize segment than vice versa. For the other segments the dependence is more symmetrical. 46% of all coal is carried on Panamaxes and coal represents 42% of the demand for Panamaxes. 20% of all coal is carried on Supramaxes and coal represents 18% of the demand for Supramaxes and so forth. As coal is a substantial part of the demand for all segments the link between the coal trade and dry bulk freight rates in the different segments is direct and clear.

If we break it down by segment, we see that 46% of all seaborne coal volumes are carried on Panamaxes, with the Cape segment in second place at 28% and Supras in third place at 20%. If we pivot and instead look at the market share of coal in each vessel segment, we see that while 28% of all seaborne coal is carried on Capesize vessels, only 16% of Capesize demand is derived from carrying coal. So, given this asymmetrical relationship you could argue that the coal trade is more dependent on the Capesize segment than vice versa. For the other segments the dependence is more symmetrical. 46% of all coal is carried on Panamaxes and coal represents 47% of the demand for Panamaxes. 20% of all coal is carried on Supramaxes and coal represents 19% of the demand for Supramaxes and so forth. As coal is a substantial part of the demand for all segments the link between the coal trade and dry bulk freight rates in the different segments is direct and clear.

Broadly speaking we have two types of coal; Coking coal and thermal coal. Coking coal aka Metallurgical coal is mainly used an energy source in steel production. The demand for metallurgical coal is thus highly correlated to the demand for steel. Thermal coal aka steaming coal is mainly used to generate electricity either to public electricity grids or directly by industry consuming electrical power (such as chemical industries, paper manufacturers, cement industry and brickwork).

Coking coal will continue to be a vital energy source for global steel production and global demand for coking coal will continue to correlate with the global growth rates in industrial production.

The thermal coal industry is without doubt under heavy pressure these days. Investors are pulling out of coal related companies in fear of association, whilst local pollution together with global warming, is affecting the public’s and policymakers’ attitude towards coal negatively. However, the rumor of coal’s death is greatly exaggerated in our view.

The chart above shows all the capacity additions and retirements since 2000 in the global thermal coal fleet in addition to thermal coal plants currently under construction or in various phases of development. The year axis represents actual start for historical periods and the scheduled start for future periods. There will be slippage in the completion year of plants currently under construction so 2020 is unlikely to record as strong growth as indicated by the graph. Given that the pipeline of projects in the coming five years is considerably lower than the actual additions in the previous 5-year period it seems very likely that the yearly capacity additions will slow down going forward. Also, we should expect retirements in the developed economies to continue at a high level as margins from coal fired electricity production is under pressure from competing sources of energy such as gas and renewable. However, while we do believe that the net growth in coal fired capacity will slow down – both in percentage terms and absolute terms – we are less confident that we will see negative growth in the coming years.

If we drill down and take a closer look at where retirements are happening and where new thermal coal plants are coming on stream the outlook for the seaborne trade looks better. Almost half of the retirements in the last 5 years have occurred in the United States, a country that is not a big coal importer due to abundant domestic coal reserves. In second place we find China with 23% of global retirements. However, new commissions in China has been five times as high in the same period, and China will without doubt continue to expand the size of their thermal coal fleet in the coming years. In third and fourth place we have the EU and the UK. The trend of high retirements in the EU is set to continue and this is the region where we are most likely to see substantial negative growth levels in coal imports going forward. The UK has decided to phase out coal entirely from the energy system in 2024. But, the positive news for the global seaborne market is that most of the fall in UK imports is already behind us and any further declines will not be significant from a global perspective. Thus, to summarize it is mostly retirements in the EU which will be a negative factor for coal imports in the coming years.

Now, let’s have a look at where the thermal coal fleet is growing. The thermal coal fleet pipeline is by far largest in China. However, nowadays there is no direct link between the size of China’s thermal coal fleet and the size of of China’s coal import. The reason is that China also has large coal reserves and the Chinese government is keeping coal imports in check to protect the profitability of domestic miners. Thus, for China there are other forces at play which we will come back to later. The region with the second largest pipeline is Emerging Asia, a region where coal imports has been growing strongly in recent years, a growth that is set to continue in the coming years. In third place comes India, where the demand for coal demand is certain to climb in the coming years. Whether that translates into higher imports or not is another question as India – similarly to China – has huge domestic coal reserves themselves. The level of coal imports will to a large extent rely on the growth rates in India’s domestic production and to what extent the coal can be delivered cost efficiently to the end users. Turkey’s import is also likely to climb higher given the size of their thermal coal fleet project pipeline. Lastly, we have the important coal importing countries of Japan and South Korea where combined imports are likely to be at least stable going forward given the size of the fleet currently in construction. Taken together we are quite confident that thermal coal imports outside of China and India will grow in the coming 3-5 years as the growth in Emerging Economies more than offsets the falling imports in developed economies (mainly EU). The swing factors for the total level of thermal coal imports will continue to be China and India.

As mentioned above the Chinese government is keeping coal imports in check to protect the profitability of domestic miners. They do this by enforcing coal import quotas on a yearly basis. The Chinese government has defined a green zone for coal prices ranging from 500 to 575 yuan per ton for the benchmark price. In this green zone the domestic coal producers and the domestic thermal coal plants are profitable (electricity tariffs are regulated). They have further defined a yellow zone and a red zone. When prices are in the red zone it will usually trigger a change in policy from the Chinese government. Coal loadings to China started of the year at very strong levels. At the same time energy demand was negatively impacted by covid-19. Domestic coal prices fell quickly and moved into the lower red zone which triggered a policy response where import quotas were strictly enforced. The consequence has been a sharp reduction in coal loadings to China since July. Coal loadings to China in September and October are the weakest in five years and is down 44% from the same period last year. The very low imports in the second half of the year has brought year to date coal loadings down 11% compared to last year. However, a combination of curtailed supply and rapidly improving energy demand has led to surging domestic coal prices, which now are in the upper red zone. The arbitrage on coal imports are huge and the only limiting factor for imports to China today is the lack of import quotas. We think it is likely that the high domestic coal price will trigger a softer stance towards import in the coming months. In recent years the coal import quotas have been renewed at the start of each calendar year. Given that the coal price currently is in the red zone we think it is unlikely that this renewal practice will be changed. We believe coal loadings to China will increase in November and December even in the absence of new quotas for 2020. The reason is that the current arbitrage on coal imports is enough to cover the demurrage for a vessel waiting to discharge for up to 6 months. Thus, traders are incentivized to load the coal today at low international coal prices and discharge in China in the new year when quotas are renewed. For 2021 we believe that Chinese imports has the potential to increase from this year as domestic coal prices are at a very high level, but this warrants a policy change from the Chinese government. Without a policy change imports will be on par with this year. We think a policy change for the worse is unlikely given that the coal price is in the red zone.

China is limiting their imports of Australian coal due to an increasingly negative bilateral relationship between the two countries. China can easily live without Australian thermal coal but will find it harder to replace Australian coking coal. It remains to be seen for how long China can maintain their hard stance on import of Australian coking coal, but it is likely to continue to be a negative factor for imports in the coming months. If the “ban” continues well into next year, then China must source their coking coal farther away which will have a positive effect on the average distance of the imports. If longer distance is enough to compensate for lower volumes remain to be seen.

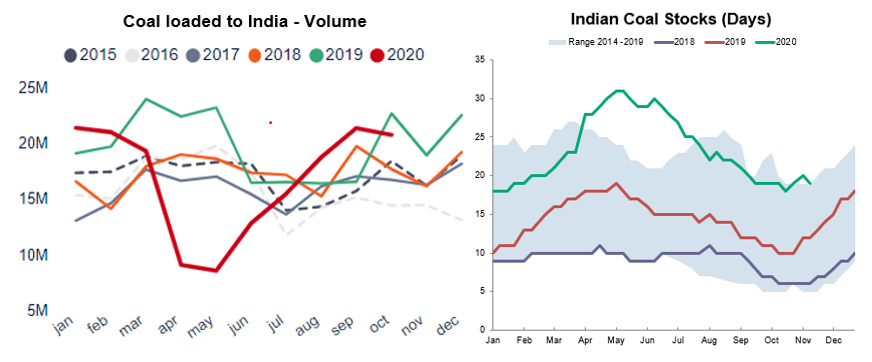

Indian coal imports were growing steadily in the last 3 years. 2020 import has been negatively impacted by the covid-19 situation. Coal loadings to India were at a high level in Q1 but nosedived in Q2 as covid-19 hit the economy. Loadings destined to India has been back on track in the last three months, but year to date loadings are still down 14%. The long-term growth levels in Indian coal imports will to a large extent hinge on whether domestic coal production can keep up with growth in coal demand. Nevertheless, for 2021 we are confident that imports will increase on the back of a post covid-19 recovery.

Coal imports in the world outside China and India has also been trending higher in recent years as the growth in Asia has more than offset declines in developed economies in the western world. South East Asian imports has grown exponentially in the last three years culminating with a year on year growth rate in imports of about 46% in 2019. Loadings of coal volumes to South East Asian nations has managed to record a solid growth of 19% year to date, in a period where the economies has been hard hit by covid-19.

We firmly believe that South Asian imports will continue to grow at a firm pace in 2021. The combined imports of the Japanese, South-Korean and Taiwanese economies has also been growing at a steady pace in recent years. Loadings to these Far East economies is down 9% in the year to date. A combination of a covid-19 recovery and an expansion of the thermal coal plant capaxity makes us fairly confident that imports in these Far East economies will grow in 2021. Coal loadings into continental Europe managed to record positive growth in 2017 and 2018 but collapsed in 2019 with a 21% negative growth. The negative trend has accelerated in 2020 with loadings down 37% year on year. The long term prospects for coal imports into the continental Europe is clearly negative but we will not be surprised if imports in 2021 manages to increase from the very weak levels in 2020 which have been dragged excessively down by covid-19.

To summarize we believe global coal imports in 2021 is likely to record quite a positive growth as the global economies recover from the black swan event of covid-19.

Next week we will take a closer look at how the fundamental drivers for grains is shaping up for 2021. In subsequent reports we will take a closer look at minor bulks and bauxite before we finish up the series with a look on the supply side.

Source: Peter Lindström, Head of Klaveness Research